Municipals were slightly firmer Thursday as U.S. Treasury yields fell and equities were better to close the session.

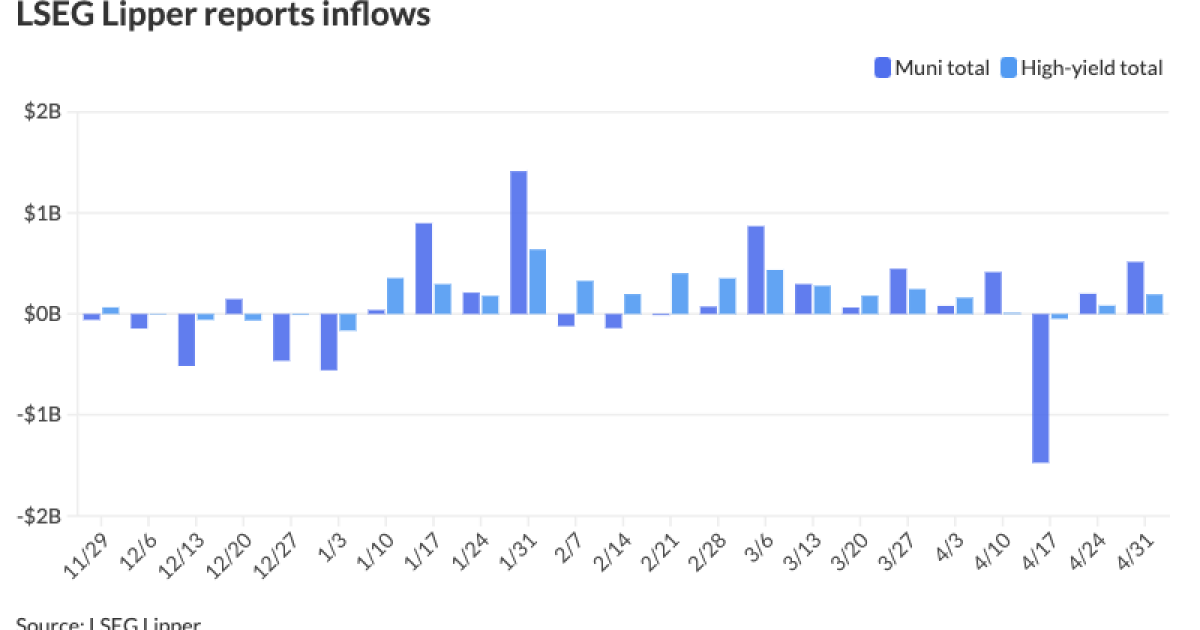

Municipal bond mutual funds saw another week of inflows as investors added $515.5 million for the week ending Wednesday after

High-yield funds also saw inflows to the tune of $189.4 million after $82.8 million of inflows the week prior, LSEG Lipper reported.

Triple-A yields fell one to three basis points while USTs were better across the curve with the best performance on the short end.

The two-year muni-to-Treasury ratio Thursday was at 65%, the three-year at 64%, the five-year at 62%, the 10-year at 61% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 64%, the three-year at 63%, the five-year at 61%, the 10-year at 61% and the 30-year at 82% at 3:30 p.m.

The Fed “took some weight off the market” Wednesday with a “less hawkish” tone that helped ease some fears, said James Pruskowski, chief investment officer at 16Rock Asset Management.

Following a “sloppy” April — the third worst in three decades — munis are in a good place with lots of “pent-up performance,” he said.

Furthermore, the “historical runway” heading into Memorial Day is favorable, rolling into the summer months of June through August, he noted.

Those months, Pruskowski said, will be “pretty bullish” regarding reinvestment potential and performance generation.

“There seems to be excellent value in muni credit spreads wide versus ratios, which are fair,” he said.

Market participants almost have “a second bite of the apple” following April and

Over the past several years, investors have been waiting for the Fed to cross the chasm “from a hawkish tightening stance to a steady stance to potentially easing stance,” he said.

It’s still unclear what type of landing there will be or whether there will be a “resurgence” of growth, he noted.

A lot of supply was added in April ahead of the uncertainty from the FOMC meeting, Pruskowski said.

However, he noted, that gave investors an opportunity to enter the market, providing those “that were willing to take risk with good reward.”

Bond Buyer 30-day visible supply is at $14.88 billion.

Barclays strategists believe issuance will fall between $32 billion to $37 billion in May, with net issuance in the range of $13 billion to $18 billion. This, they noted, does not include the $11 billion in coupon payments.

In the competitive market Thursday, the University of Massachusetts Building Authority (Aa2/AA-/AA-/) sold $150.48 million of senior project revenue bonds, Series 2024-1, to BofA Securities, with 5s of 11/2025 at 3.22%, 5s of 2029 at 2.77%, 5s of 2034 at 2.77%, 5s of 2039 at 3.33%. 5s of 2044 at 3.79%, 5s of 2049 at 4.06% and 5s of 2054 at 4.11%, callable 5/1/2034.

The Washoe County School District, Nevada, (Aa3/AA//) sold $130 million of limited tax GO school improvement bonds, Series 2024A, to Jefferies, with 5s of 6/2026 at 3.32%, 5s of 2029 at 2.97%, 5s of 2034 at 3.00%, 5s of 2039 at 3.46% and 4s of 2044 at 4.23%, callable 6/1/2034.

The Nauset Regional School District, Massachusetts, sold $120.5 million of unlimited tax GO school bonds, to Mesirow Financial, with 5s of 2025 at 3.25%, 5s of 2029 at 2.65%, 4s of 2034 at 2.85%, 4s of 2039 at 3.56%, 4s of 2044 at par and 4s of 2049 at 4..25%, callable 5/15/2032.

AAA scales

Refinitiv MMD’s scale was bumped two to three basis points: The one-year was at 3.40% (-2) and 3.20% (-2) in two years. The five-year was at 2.83% (-2), the 10-year at 2.80% (-2) and the 30-year at 3.93% (-3) at 3 p.m.

The ICE AAA yield curve was bumped one to two basis points: 3.39% (-2) in 2025 and 3.21% (-1) in 2026. The five-year was at 2.84% (-1), the 10-year was at 2.81% (-1) and the 30-year was at 3.88% (-1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was bumped two to three basis points: The one-year was at 3.43% (-3) in 2025 and 3.20% (-3) in 2026. The five-year was at 2.82% (-2), the 10-year was at 2.81% (-3) and the 30-year yield was at 3.91% (-3), according to a 3 p.m. read.

Bloomberg BVAL was bumped two to three basis points: 3.44% (-2) in 2025 and 3.24% (-2) in 2026. The five-year at 2.77% (-2), the 10-year at 2.75% (-2) and the 30-year at 3.92% (-3) at 3:30 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.880% (-7), the three-year was at 4.721% (-8), the five-year at 4.573% (-7), the 10-year at 4.578% (-5), the 20-year at 4.825% (-3) and the 30-year at 4.726% (-2) at 3:45 p.m.

FOMC redux

The Federal Open Market Committee meeting statement and Fed Chair Jerome Powell’s press conference did not strike the hawkish tone the market expected, analysts said, and should be positive for bonds.

“Our base case remains that the economy is heading for a soft landing,” said Brian Rose, senior U.S. economist at UBS Global Wealth Management. “We expect growth to moderate and inflation to slow in the months ahead, allowing the Fed to start trimming rates in September.”

UBS remains hawkish on “quality bonds.”

“Robust economic growth and elevated inflation have driven bond yields higher in recent months, improving potential returns for investors in quality fixed income,” Rose added. “Investors can benefit from attractive yields and potential capital gains if yields fall (as we expect) and diversify portfolios against equity market risks.”

BNP Paribas’ Markets360 team read Powell’s press conference “as unequivocally dovish.”

In addition to asserting policy is restrictive, he “downplayed the importance of wage growth in the overall inflation process and minimized loosening financial conditions, noting that while growth has remained steady, it has not accelerated,” they said.

Janus Henderson believes “policy is doing its job, albeit slower” than in 2023. “The normalization process back to their 2% goal will clearly take longer than many anticipated but we think patience is the right approach.”

But the dovishness “implies that the Fed implicitly accepts 3% inflation rather than aggressively trying to hit its 2% goal,” said José Torres, senior economist at Interactive Brokers. This limits the odds of recession, he noted.

“Despite setbacks on the inflation front, the May press statement does not come across as excessively hawkish, as some had anticipated,” said Christian Scherrmann, DWS U.S. economist. “Central bankers have chosen to express a degree of optimism, now viewing the risks associated with achieving their objectives as balanced. This implicitly suggests that they are not overly perturbed by recent inflation data, clearly indicating that rate cuts remain a viable option for 2024.”

“Powell struck a clearly dovish tone,” said Josh Jamner, investment strategy analyst at ClearBridge Investments, “which sparked a rally in risk assets as many investors were positioned for and fearful of a more hawkish bent after a string of hot inflation prints so far this year.”

But Chris Low, chief economist at FHN Financial, said the press conference “was nicely balanced.” While Powell acknowledged inflation accelerated in the past three reads, he showed confidence it will fall again.

“Bond yields rose early on, when Powell acknowledged three months of bad inflation news suggests the increase was real, but yields dropped back again on Powell’s confidence inflation will fall,” Low said.

Still, S&P Global Ratings Chief U.S. Economist Satyam Panday said the agency now expects a December rate cut instead of July, “conditional on economic growth and inflation pressures slowing.”

With an expected slowing economy next year, he said, “we still think the Fed is likely to pick up the pace of easing in 2025,” with four cuts.

While the higher-for-longer scenario continues, John Lloyd, lead of multi-sector credit strategies and portfolio manager at Janus Henderson Investors, said the Fed was “careful to not let the market think the next move will be anything but a cut.”

The markets, he said, “were bracing for a more hawkish Fed undertone with maybe even a mention of the word ‘hike,’ given the recent string of tough inflation prints we’ve seen to start 2024.”

But the March Summary of Economic Projections’ “three cuts for 2024 was too aggressive, and base case may move closer to zero to one cut,” Lloyd said.

“It has become abundantly clear and acknowledged by the Fed that they have more work to do, but they continue to believe that inflation will resume its downward trajectory as the year progresses,” he continued. “Whether time is enough to solve the inflation riddle remains to be seen.”

Gary Siegel contributed to this story.